|

|||||||||||||||||||||||||||||||

|

Looking at rental statistics for Seattle, take a look at current pricing in Phinney Ridge, Lake City and Newcastle compared to a decade ago.

|

Seattle Rental Market Statistics: 2002 vs. Today

February 3, 2013 By Leave a Comment

The Ten Commandments of Home Buying

January 16, 2013 By Leave a Comment

A friend recently asked me for mortgage advice. I explained how to shop around for a good rate, and then I added my catchphrase: “You didn’t ask, but…”

A friend recently asked me for mortgage advice. I explained how to shop around for a good rate, and then I added my catchphrase: “You didn’t ask, but…”

Like anyone involved in the world of finance, I’ve seen a lot of serious mortgage trouble in the last few years. Even though the days of jumbo loans with no proof of income are long gone, it’s still a homebuyer’s responsibility to make sure that taking on a mortgage doesn’t put them in the financial danger zone.

So, I told my friend, before making the leap, to work through the following checklist and make sure you’re on the good side of each rule.

Now, nobody’s perfect, and if your online dating profile says you’re looking for a financially prudent partner who fulfills every qualification below, you’ll stay lonely. “You obviously can’t do all the things on your list,” says Jane Hodges, author of Rent vs. Own.

But whenever someone has come to me in danger of losing their house, they’ve ignored nearly every single rule, including the most important one: In Mint’s recent money mistakes survey, 20% of you admitted to spending more than 30% of your income on housing.

And since January is all about fixing those pesky Money Boo Boos, and paying too much for housing is definitely a big money mistake, let’s talk about the ten commandments of home buying:

1. Don’t bite off more mortgage than you can chew

The classic lending guideline says your principal, interest, property tax, and insurance (PITI) should amount to no more than 28% of your gross income.

Obviously, that’s an arbitrary number. Your financial world won’t explode if you stretch to 29% or 33%.

But an outsized mortgage payment is going to bite you sooner or later. As we’ve seen again and again over the last four years, lenders aren’t cuddly and understanding. They just want you to make your payments, month after month.

There’s also the duration of the mortgage to consider. “Another metric is your age,” says Hodges. “If you’re 55 and a first-time buyer, you better be getting a 15-year loan, right?”

2. Have at least one steady income in the family

It’s not 2006 anymore, and banks are a lot more scrupulous about checking to see if you have any income before shoveling a houseload of money in your direction.

But it’s still your responsibility to make sure you have a steady paycheck to go with your steady mortgage payment.

3. Carry few or no other debts

A reasonably sized mortgage quickly becomes an unreasonable burden when you mix it with student loans, car loans, and credit card debt.

The traditional lending guideline says that your mortgage payment (yes, including interest, tax, and insurance) and all your other debts should add up to 36% of your income or less.

Again, I’ve had people show me their monthly budget, and 70% of their income was going to debt repayment. That can’t end well.

4. Keep a big buffer

On top of debt repayment, you have other non-negotiable bills every month: utilities, insurance, a basic level of food and clothing, and maybe a tuition payment. Then there are discretionary expenses: saving, dining out, entertainment, travel, etc.

In their book, All Your Worth, Elizabeth Warren and Amelia Warren Tyagi recommend that you keep your non-discretionary expenses to less than 50% of your take-home income.

Like the other percentages we’ve been throwing around, this one isn’t magic, but it’s a nice guideline. When too much of your income gets sucked into required expenses, you lose flexibility.

A brief period of unemployment, a medical emergency, or a car repair can turn into a financial disaster that ultimately costs you your house.

5. Have an emergency fund

If you have a well-stocked emergency fund now, don’t drain it to fund a down payment. If you don’t have one, you’re not ready for a mortgage, no matter how perfect a Cape Cod you just toured.

6. Have good life, disability, and health insurance

If you’re uninsured or underinsured, you’re in no position to buy a house, unless you’re sitting on a giant pile of money. Are you?

7. Bring a 20% down payment

Small down payments lead to big problems. Reuters’ Felix Salmon crunched the numbers last year and found that mortgages with a 15%-20% down payment were more than twice as likely to become delinquent as mortgages with a 20% down payment for most years before the financial crisis.

Lower down payments did much worse. His conclusion: “So, let’s all remember this chart the next time anybody claims that you can have a safe mortgage with a low down payment. Because the fact is that you can’t.”

8. Don’t use home equity as part of your retirement plan

Home equity is great—that’s why you should bring a big down payment. But it’s also undiversified, subject to the ups and downs of the real estate market, and hard to quickly turn into cash.

It’s fine to have your retirement savings plan reflect the fact that your mortgage will be paid off in retirement and your ongoing housing costs will be low (although, you’ll still be on the hook for maintenance, property tax, and insurance).

If you’re assuming your house will appreciate at a lavish rate and you’ll be able to cash out later when you downsize, think again: over the long term, house prices rise at about the rate of inflation, according to the Case-Shiller index.

9. Be prepared to settle down

Unless you’re prepared to stay in your house for seven to ten years, the costs of buying and selling are likely to swamp any price appreciation.

Put more simply: If you move a lot, you’re better off renting. And most people underestimate how soon they’ll want to (or need to) move. Look at your past behavior and be realistic.

10. Check the price-rent ratio for signs of a bubble

A couple of times a year, Trulia.com looks at housing markets nationwide and declares them under-, over-, or well-priced based on the historical price-rent ratio, which is just the price of a house divided by the annual rent for an equivalent house.

During the housing bubble, prices in many markets rose to absurd levels by this standard: People were buying $500,000 houses that would have rented for, say, $20,000/year.

In retrospect, this obviously wasn’t going to work out. Prices in most markets are now sane (ratio of 15 or less), but you should still look at the neighborhood level. My Seattle neighborhood, for example, is still looking a little hot.

Source: Matthew Amster-Burton via: Mint.com

Rental Demand to Edge Higher in 2013?

January 2, 2013 By Leave a Comment

Five to six million new renter households may be created within the next 10 years, likely caused from low inventories of homes available and tight credit conditions, according to the Bipartisan Policy Center.

Five to six million new renter households may be created within the next 10 years, likely caused from low inventories of homes available and tight credit conditions, according to the Bipartisan Policy Center.

Rental demand is expected to particularly increase among seniors looking to downsize their homes, as well as young adults and a growing immigrant population.

“We expect to see an increase in household formation and for a variety of reasons that household formation is likely to be more heavily concentrated among renters and households who are likely to be renters for somewhat longer than was the case for the last 20 years,” Barry Zigas, director of Housing Policy for Consumer Federation of America, told HousingWire.

Tight credit conditions continues to be one main culprit holding back home ownership among some potential buyers.

“Credit for home ownership borrowing will likely be tighter and potentially more expensive, relative to earlier times,” Zigas predicts. “Families will likely have less wealth because the rising generation is starting with less wealth. If down payments are at any significant level, it will be a barrier to acquiring a home for longer than may have been the case in the past.”

Source: “Small Housing Inventory May Push Rental Demand for Years,” HousingWire

Real Estate as a Hedge Against Inflation

January 1, 2013 By Leave a Comment

Why do houses appreciate? It’s not because they get better with time because they most certainly don’t. They can actually get pretty worn out and require substantial repairs. So then what causes the famous appreciation so many people buy houses for?

Why do houses appreciate? It’s not because they get better with time because they most certainly don’t. They can actually get pretty worn out and require substantial repairs. So then what causes the famous appreciation so many people buy houses for?

Inflation.

The CNN news headline on TV this morning was “America’s economy held hostage!” Merry Christmas everyone, we’re all doomed. At least that seems to be the talk now that the holidays are over and consequently we have nothing better to focus on except this thing they call the Fiscal Cliff. If you haven’t heard that term you are obviously living in hole. It’s on every news channel, in every paper, and I’m actually surprised more sitcoms haven’t made fun of the potential loom that hangs over us.

What is Inflation and Why Do We Need a Hedge?

What does the Fiscal Cliff mean for all of us? I really don’t know nor am I going to try to analyze it here. I am certainly going to hope for the best but I wouldn’t question you if you say we are all doomed either. I do know one thing though: more than ever, I know it’s time for me to be in control of my money. I don’t claim to be a financial expert by any stretch but I do know that if inflation is going to continue, which follows right along with this Fiscal Cliff idea, I want to be smart with my money by keeping it as protected against inflation as I can.

What does the Fiscal Cliff mean for all of us? I really don’t know nor am I going to try to analyze it here. I am certainly going to hope for the best but I wouldn’t question you if you say we are all doomed either. I do know one thing though: more than ever, I know it’s time for me to be in control of my money. I don’t claim to be a financial expert by any stretch but I do know that if inflation is going to continue, which follows right along with this Fiscal Cliff idea, I want to be smart with my money by keeping it as protected against inflation as I can.

Thinking in terms of Inflation for Dummies, inflation basically means:

- More money is created

- The value of the dollar goes down

- Therefore prices go up

I have $100. The government prints more money. What I can now buy with my $100 is what I could have bought with only $80 before the new money was printed. Translate that to a real-world example: A gallon of milk in 1970 cost roughly $1.15. Today a gallon of milk is about $4.00.

Hello, inflation, it’s nice to meet you.

There are a lot of factors in thinking about where the safest places for your money are. Stocks, CDs, banks, real estate, commodities, under your mattress, in outer space…everyone has different opinions. I’m not here to say what is right or wrong about each option, but I am here to explain how real estate can protect against this little witch we call inflation.

How Real Estate Can Fight Inflation

Real estate is one of the few assets that react proportionately to inflation. As inflation occurs, housing values go up and rents go up. Can you then see why owning real estate may be a good thing? If not, let’s put this into perspective with a simple hypothetical example.

In 2012, you buy a house for $100,000. After the world doesn’t end that year and the government begins to drive off the Fiscal Cliff, the financial markets become a mess and inflation is in full-bloom for the next 10 years. Now 10 years later, because of inflation, this same house is worth $180,000. You now own an $180,000 house that you only had to pay $100,000 for! Sounds like a deal to me. You basically have $80,000 in free dollars now.

Inflation: The Landlord’s Friend?

Let’s take this up another notch. Instead of living in the house yourself, you decide to rent it out and you begin collecting $1,000/month in rent. At $1,000/month you net $300 after the mortgage and other expenses. At the end of a 10-year stint with no inflation, you would have pocketed $36,000 in passive income (woot!). However, thanks to the same inflation that jumped the house’s value over those 10 years, you had to increase the monthly rent by $100 every other year. This would put the amount of passive income you pocketed at $50,000 instead of $36,000 (double-woot!). Although that $50,000 doesn’t take into account any increases to property taxes, insurance, etc., so l am going to put it back down at $45,000 before someone argues me on that one. Regardless, inflation has just put a nice extra chunk of cash in your pocket! $9,000 specifically in this case.

One property in only 10 years, thanks to inflation, has put $89,000 in your pocket you wouldn’t have otherwise had. Actually, it would be more than that once you consider how much you reaped in tax benefits as well, but I’m trying to keep it simple.

Note: Going along with the idea of trying to keep it simple, I acknowledge that I have ignored a lot of factors here associated with appreciation, taxes, income and expenses, but the point is to focus solely on the impact of inflation and nothing else. I also didn’t go with any particular % inflation either but rather used simple numbers to show the point.

If inflation occurs, real estate is one of the only inflation-adjusted assets other than commodities. While most of the population believes real estate is a risky investment, I believe real estate is one of the only safe investments left given our continuing financial crisis.

source: BiggerPockets

Pending Home Sales Rise Again

December 28, 2012 By Leave a Comment

Pending home sales increased in November for the third-straight month and reached the highest level in two-and-a-half years, according to the National Association of REALTORS®.

Pending home sales increased in November for the third-straight month and reached the highest level in two-and-a-half years, according to the National Association of REALTORS®.

The Pending Home Sales Index, a forward-looking indicator based on contract signings, rose 1.7 percent to 106.4 in November from a downwardly revised 104.6 in October and is 9.8 percent above November 2011 when it was 96.9. The data reflect contracts but not closings.

The index is at the highest level since April 2010, when it hit 111.3 as buyers were rushing to beat the deadline for the home buyer tax credit. With the exception of several months affected by tax stimulus, the last time there was a higher reading was in February 2007 when the index reached 107.9.

Lawrence Yun, NAR chief economist, said home sales are on a sustained uptrend. “Even with market frictions related to the mortgage process, home-contract activity continues to improve. Home sales are recovering now based solely on fundamental demand and favorable affordability conditions.”

On a year-over-year basis, pending home sales have risen for 19 consecutive months.

The upward momentum means existing-home sales should rise 8 to 9 percent in 2013 to approximately 5.1 million, following a 10 percent gain expected for all of 2012. The median existing-home price is projected to rise just over 4 percent in 2013, after rising more than 7 percent in 2012.

The PHSI in the Northeast rose 5.2 percent to 83.3 in November and is 15.2 percent above a year ago. In the Midwest the index edged up 0.1 percent to 103.8 in November and is 15.2 percent above November 2011. Pending home sales in the South were unchanged at an index of 117.2 in November and are 13.9 percent higher than a year ago. In the West (see Greater Seattle stats) the index rose 4.2 percent in November to 110.1, but is 3.2 percent below November 2011 with inventory constraints limiting sales.

Source: NAR

What is Ahead for Housing?

December 20, 2012 By Leave a Comment

5.9 Million young adults living with their parents! This trend is out of line with historical norms. As the economy continues to improve, we will see this number change.

![clip_image002[5]](http://www.emmanuelfonte.com/wp-content/uploads/2012/12/clip_image0025.jpg "clip_image002[5]")

The reality is that those young adults DO want to own their own home. The dream of home ownership has been impacted by the economic challenges faced over the past few years. This desire will come to fruition moving forward.

![clip_image002[7]](http://www.emmanuelfonte.com/wp-content/uploads/2012/12/clip_image0027.jpg "clip_image002[7]")

The data also tells us that those young adults are forming households and getting back out on their own. Human nature desires for autonomy and the ability to set up our own place.

![clip_image002[9]](http://www.emmanuelfonte.com/wp-content/uploads/2012/12/clip_image0029.jpg "clip_image002[9]")

Many have made the argument that renting is better than owning. While for some that may be true depending on their location, time they will be in said location, life circumstances, the numbers have swung back to owning as the way to go for many.

While no one wants to return to the frenzy of 2003-2005, we are seeing in many markets a flip towards a seller controlled market. Buyers need to be ready to pull the trigger when the right place is available for them.

Let me know how I can help. Email me.

source: KCM

Buyer Urgency Expected to Drive 2013

December 19, 2012 By Leave a Comment

Home shoppers will likely have more urgency in the new year, wanting to buy before home prices rise even more.

Home shoppers will likely have more urgency in the new year, wanting to buy before home prices rise even more.

Home prices are edging up in most markets, and buyers are taking notice. Buyer surveys recently have shown that home shoppers expect home prices to continue to inch up, and they want to cash in before they rise too much higher.

“Every single thing about housing is flashing green” with household formation rising, inventory falling, and affordability hovering at record highs, James Dimon, chief executive of J.P. Morgan Chase told CNBC last month.

In 2013, rising rents are expected to push more renters to buy, The Wall Street Journal reports. Also, investors who’ve had a big appetite for housing in recent years may start to decrease their share in some markets that have seen prices rise, such as Phoenix, and focus on other markets still in recovery mode, like Chicago and Atlanta.

“Rising prices could eventually encourage more sellers to put their homes on the market, which would help boost demand even further,” The Wall Street Journal reports.

To meet the expected increase in demand in 2013, some real estate companies are going on a hiring spree. For example, Redfin says it plans to increase its 400 agents nationally by 50 percent by the end of January after having to send about half of its referrals to other companies earlier this year because demand outstripped its supply of agents.

Source: “2013: How Rising Prices Could Boost Housing Demand,” The Wall Street Journal

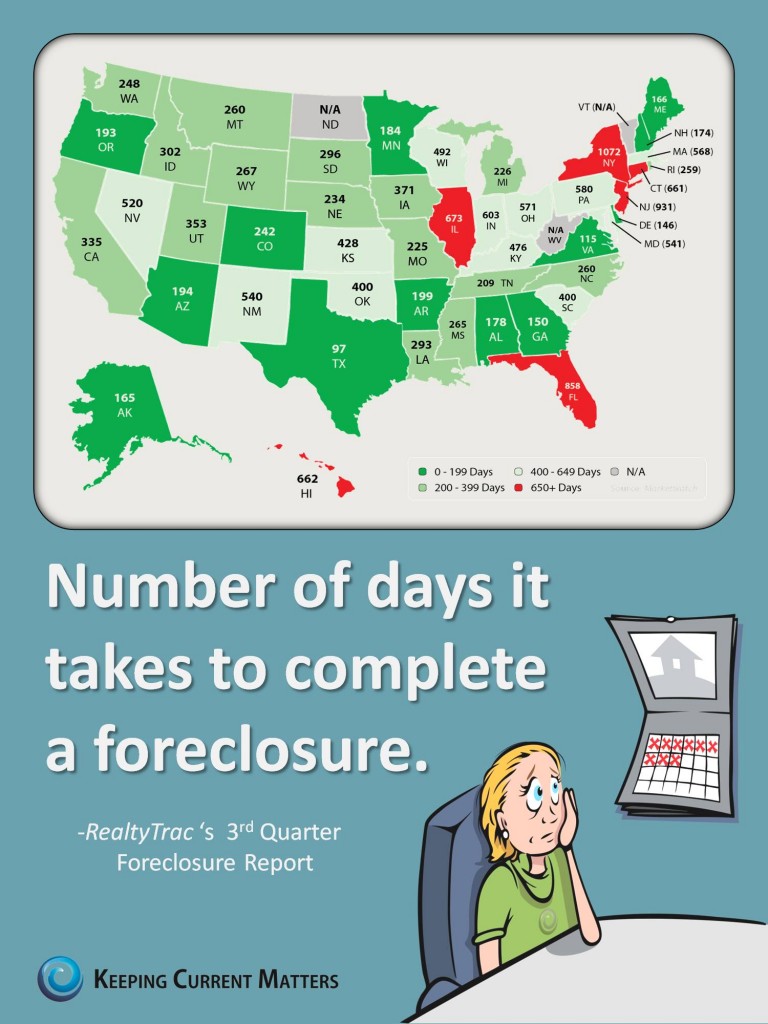

Time It Takes to Complete a Foreclosure [INFOGRAPHIC]

December 14, 2012 By Leave a Comment