Freddie Mac recently released its U.S. Economic and Housing Market Outlook through March showing that as we head into the spring home buying season, continued low mortgage rates, increasing house prices, and gradually improving consumer confidence will help support increased home sales. A short preview video and the complete March 2013 U.S. Economic and Housing Market Outlook are available here.

Freddie Mac recently released its U.S. Economic and Housing Market Outlook through March showing that as we head into the spring home buying season, continued low mortgage rates, increasing house prices, and gradually improving consumer confidence will help support increased home sales. A short preview video and the complete March 2013 U.S. Economic and Housing Market Outlook are available here.

Outlook Highlights

• Compared to 2012, expect home sales to be up 8 to 10 percent for 2013.

• Expect housing starts to increase to 950,000 units for 2013, compared to 780,000 in 2012.

• In 2012, real estate added $1.5 trillion to balance sheets, and residential mortgage debt outstanding increased by 0.1 percent in the fourth quarter of 2012, indicating household deleveraging might be drawing to a close.

• Because of sequestration spending reductions, expect the unemployment rate in 2013 to average about 7.8 percent, essentially flat for the year or about 0.25 percentage points higher than it otherwise would have been.

• Regardless, the housing wealth effect is taking hold in the broader market which should translate into the healthiest spring home buying season since 2007.

“History shows us not all economic recoveries are created equal and consumer confidence mirrors this fact,” says Frank Nothaft, Freddie Mac vice president and chief economist.

“With the spring home buying season upon us, the recent highs in the stock market are a welcome signal of better times ahead. But it will be the gradually declining unemployment rate and steadily improving housing market that will deliver broad-based economic benefits for Americans and, in turn, support the overall recovery.”

For more information, visit www.FreddieMac.com

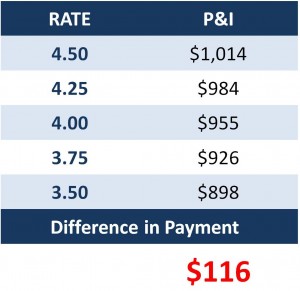

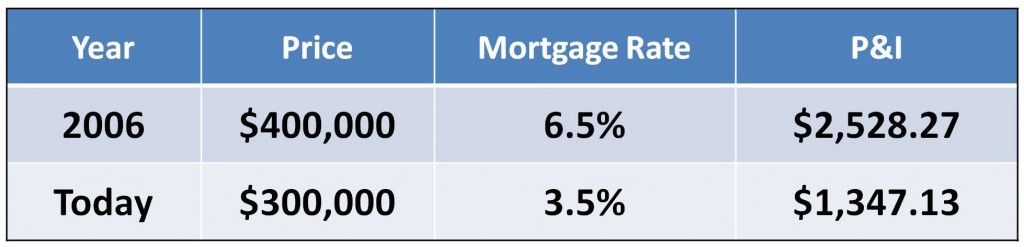

A big component in the cost of a home is the mortgage interest rate a purchaser pays. Understanding where rates are headed will help in making a decision whether to buy now or wait.

A big component in the cost of a home is the mortgage interest rate a purchaser pays. Understanding where rates are headed will help in making a decision whether to buy now or wait.