The Millennial generation is about 90 million strong—forming the largest demographic wave in the country’s history—and some reports suggest they’re readying for home ownership.

The Millennial generation is about 90 million strong—forming the largest demographic wave in the country’s history—and some reports suggest they’re readying for home ownership.

Millennials’ entrance into home ownership has been delayed due to the recession, high unemployment, and high student loan debt. They’ve been living in their parents’ homes, as well as delaying marriage and having children, surveys show. But the pent-up demand from this generation is starting to surface, says Fred Ehle, vice president for PulteGroup.

Homebuilders, like PulteGroup and Better Homes and Gardens Real Estate, recently revealed surveys of what Millennials want in their future homes. In general, the surveys reveal that this generation isn’t wowed by luxury and prefers technology and flexible space.

Pulte Homes found in its research that more than half of Millennials who decided to buy a home last year from the homebuilder said their main reason was to invest and build equity.

As for what they’re looking for in a home, they appreciate an efficient use of space, an open layout for entertaining, ample storage space, and outdoor space that extends their living areas, according to the Pulte survey of 531 adult renters between the ages of 18 and 34.

“What may be different about this buyer is that they may have more stuff,” says Fred Ehle, vice president for PulteGroup. “It’s different kind of stuff: technological gadgets, gaming. They also do work from home.”

The Better Homes and Gardens survey of 1,000 adults ages 18 to 35 found that Millennials don’t like traditional floor plans and prefer unique spaces. They like to do home improvements themselves and are “fix-it” types.

One in five said that “home office” is a better suited name for their dining room, according to the Better Homes and Gardens survey. What’s more, 43 percent said they want to transform their living room into a home theater.

The survey also showed they’d rather have extra space in their kitchen for a TV than a second oven. Nearly two-thirds of those surveyed say they wouldn’t purchase a home without up-to-date tech capabilities.

Source: “GenY is finally in a mood to buy (houses),” USA Today

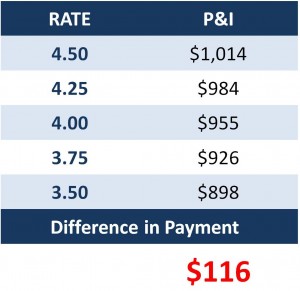

A big component in the cost of a home is the mortgage interest rate a purchaser pays. Understanding where rates are headed will help in making a decision whether to buy now or wait.

A big component in the cost of a home is the mortgage interest rate a purchaser pays. Understanding where rates are headed will help in making a decision whether to buy now or wait.