What Impact Will Increasing Mortgage Rates Have On Prices?

January 14, 2014 By Leave a Comment

Many pundits are warning that there will be a drop in real estate values because mortgage rates are beginning to increase. The logic makes sense. However, history shows that increasing rates have not negatively impacted home values in the past.

Many pundits are warning that there will be a drop in real estate values because mortgage rates are beginning to increase. The logic makes sense. However, history shows that increasing rates have not negatively impacted home values in the past.

Four times over the last 30 years mortgage interest rates have dramatically increased. Here is the impact the increases had on home values at the time:

Dates |

Mortgage Rate |

Home Values |

| May ‘83 – July ‘84 |

12.63 – 14.67 |

+ 6.6% |

| March – Oct ‘87 |

9.04 – 11.26 |

+ 5.2% |

| Oct ’93 – Dec ‘94 |

6.83 – 9.2 |

+ 1.2% |

| April ’99 -May 2000 |

6.92 – 8.52 |

+ 10.9% |

Perhaps the impact of increasing rates on future home prices won’t be as dramatic as some are predicting.

What You Must Know About Home Appraisals

August 28, 2013 By Leave a Comment

Understanding how appraisals work will help you achieve a quick and profitable refinance or sale.

Understanding how appraisals work will help you achieve a quick and profitable refinance or sale.

1. An appraisal isn’t an exact science

When appraisers evaluate a home’s value, they’re giving their best opinion based on how the home’s features stack up against those of similar homes recently sold nearby. One appraiser may factor in a recent sale, but another may consider that sale too long ago, or the home too different, or too far away to be a fair comparison. The result can be differences in the values two separate appraisers set for your home.

2. Appraisals have different purposes

An appraisal being used to figure out how much to insure your home for or to determine your property taxes may rely on other factors and arrive at different values. For example, though an appraisal for a home loan evaluates today’s market value, an appraisal for insurance purposes calculates what it would cost to rebuild your home at today’s building material and labor rates, which can result in two different numbers.

Appraisals are also different from CMAs, or competitive market analyses. In a CMA, a real estate agent relies on market expertise to estimate how much your home will sell for in a specific time period. The price your home will sell for in 30 days may be different than the price your home will sell for in 120 days. Because real estate agents don’t follow the rules appraisers do, there can be variations between CMAs and appraisals on the same home.

3. An appraisal is a snapshot

Home prices shift, and appraised values will shift with those market changes. Your home may be appraised at $150,000 today, but in two months when you refinance or list it for sale, the appraised value could be lower or higher depending on how your market has performed.

4. Appraisals don’t factor in your personal issues

You may have a reason you must sell immediately, such as a job loss or transfer, which can affect the amount of money you’ll accept to complete the transaction in your time frame. An appraisal doesn’t consider those personal factors.

5. You can ask for a second opinion

If your home appraisal comes back at a value you believe is too low, you can request that a second appraisal be performed by a different appraiser. You, or potential buyers, if they’ve requested the appraisal, will have to pay for the second appraisal. But it may be worth it to keep the sale from collapsing from a faulty appraisal. On the other hand, the appraisal may be accurate, and it may be a sign that you need to adjust your pricing or the size of the loan you’re refinancing.

Our Changing Housing Market

August 4, 2013 By Leave a Comment

The housing market has changed a lot over the last 40 years, with the number of home sales, the size of homes, and the cost of homes all changing since the 1970s. Check out this great infographic below to see the ups, and downs, of the housing market over the last 40 years.

source: MitchellHomesInc.com

source: MitchellHomesInc.com

Household Formation: Pent-Up Demand Is High

August 3, 2013 By Leave a Comment

The current rate of household formation in the United States is still well below the expected trend and faulted as a major culprit for “pent-up demand.” According to an analysis by Trulia, an online residential real estate site, potentially 2.4 million households are hitting the pause button. The majority of that number is comprised of young people between the ages of 18 and 34 who have delayed moving out on their own for a variety of reasons.

The current rate of household formation in the United States is still well below the expected trend and faulted as a major culprit for “pent-up demand.” According to an analysis by Trulia, an online residential real estate site, potentially 2.4 million households are hitting the pause button. The majority of that number is comprised of young people between the ages of 18 and 34 who have delayed moving out on their own for a variety of reasons.

An average of 1.1 million new households are formed each year in the United States. But from the first quarter of 2008 to the first quarter of 2011, just 450,000 new households have been added on an annual basis. This sluggish rate means a decrease in the overall demand for housing, which affects the annual construction rate. But this “pent-up demand” driven by young adults who are still living at home or doubling up with roommates is bound to give way, say some housing experts.

Will household formation increase sooner or later? Housing Wire is optimistic, reporting that the conditions are better today for emerging households. Steady job growth over the last several years is a good sign. Sterne Agee analyst Jay McCanless says, “We believe steady, if unremarkable, monthly job growth is creating a…household formation environment for 2013 which should support our positive housing outlook.”

If that projection holds true, increased demand is merely a matter of time. When households come out of hiding looking for single- and multi-family residences or apartments, they could potentially inundate the market.

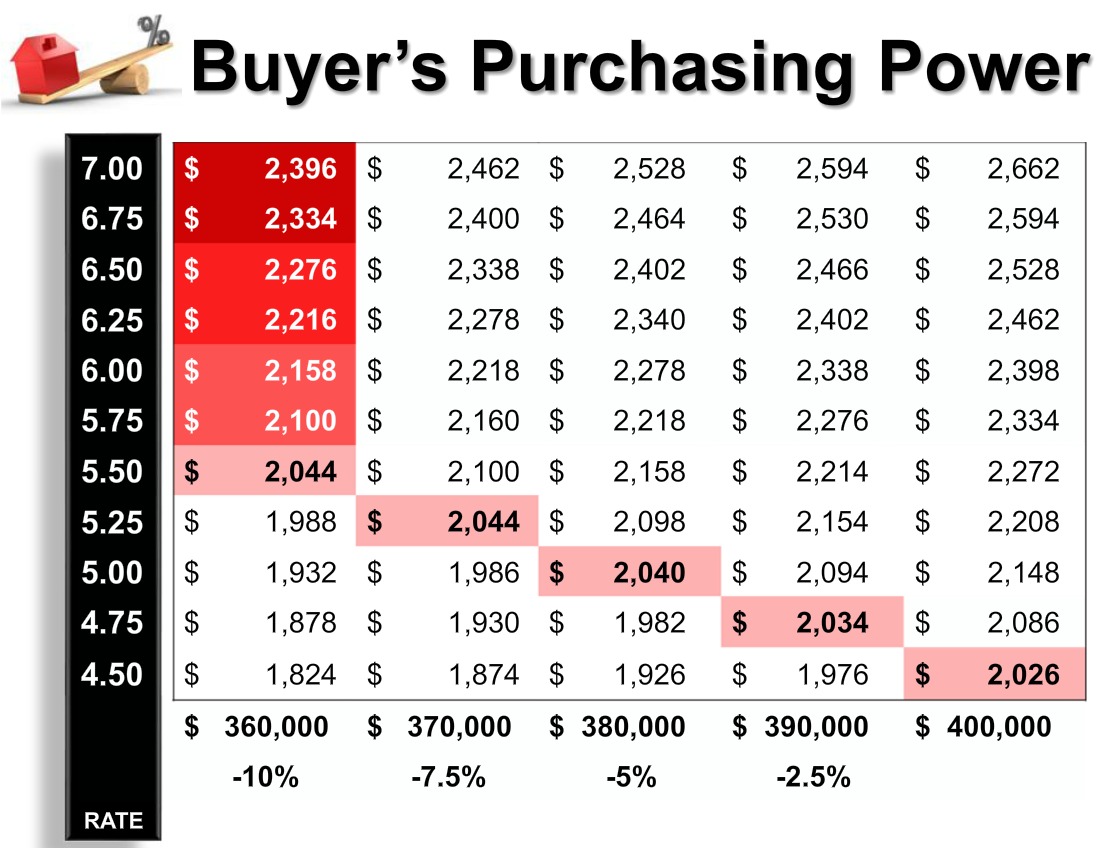

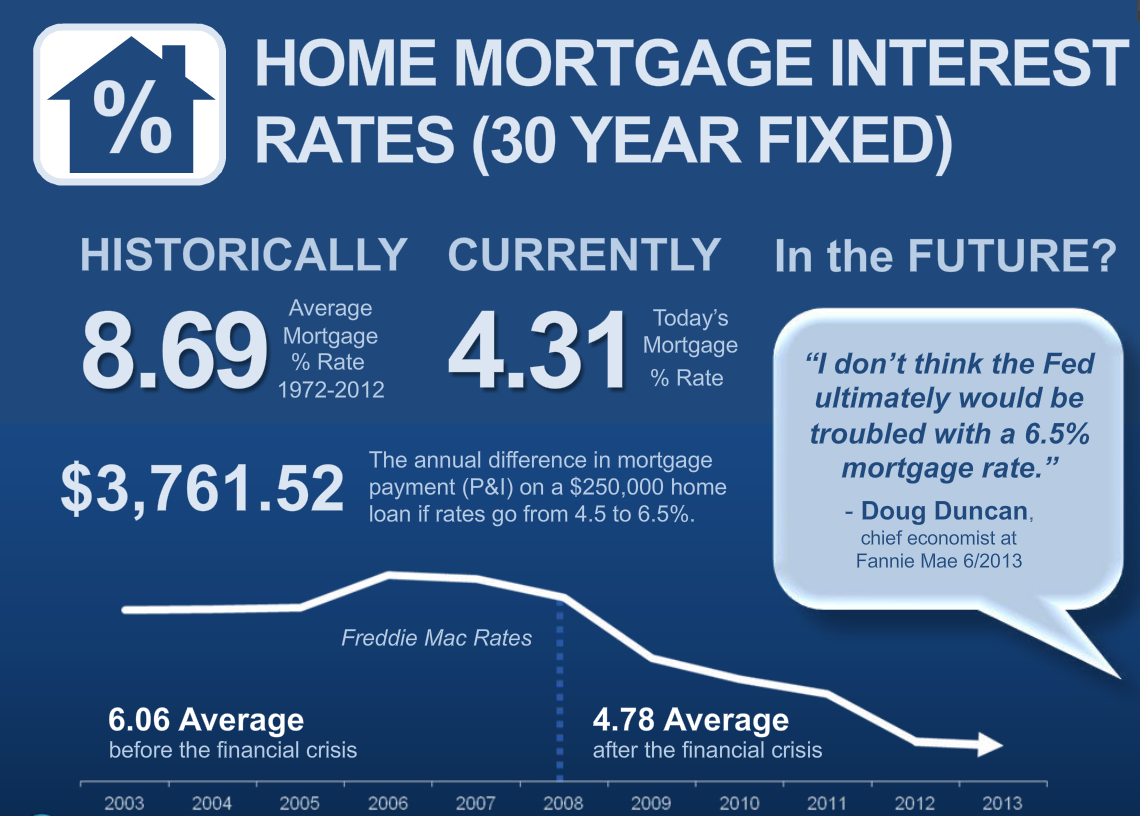

Is It Time To Buy? If Interest Rates Matter To You, It Is

July 25, 2013 By Leave a Comment

The question on so many home buyer’s minds is, “is it time to buy?” In some circumstances it is. For those requiring a mortgage, the rates available today would indicate it’s time.

Those rates impact buying power. Here’s a simple chart demonstrating what interest rates increasing does to buying power.

Those rates impact buying power. Here’s a simple chart demonstrating what interest rates increasing does to buying power.

As a seller, this is why it is important to price at market value. The longer you stay on market, the buyer pool of your home may shrink due to these rates.