Figuring out whether it’s better to buy or rent rests on three main factors: where you live, how long you plan to stay and how home prices compare to rents in the area. Real estate website Trulia analyzed data from 100 major metro areas to help determine that last factor.

Figuring out whether it’s better to buy or rent rests on three main factors: where you live, how long you plan to stay and how home prices compare to rents in the area. Real estate website Trulia analyzed data from 100 major metro areas to help determine that last factor.

See where Seattle ranks. Look for homes in Seattle.

While markets vary wildly, prices are so reasonable and interest rates so low that buying is the better option in most major U.S. cities, said Jed Kolko, Trulia’s chief economist. Nationwide, home buyers who remain in their homes for three years will save an average of 19 percent over renting. If they hold onto their homes for 7 years, the savings advantage grows to 44 percent.

That means all of the initial transaction costs of buying — the broker’s commission, title insurance, legal fees and other closing costs — will be offset by benefits, like tax write-offs and price appreciation. And those costs will become cheaper than the total costs of renting, which include insurance and agent commissions.

But the math is changing. Home prices rose 7 percent year-over-year last month while rents went up only 3.2 percent, according to Trulia. “Buying is still cheaper than renting but the gap is closing,” said Kolko.

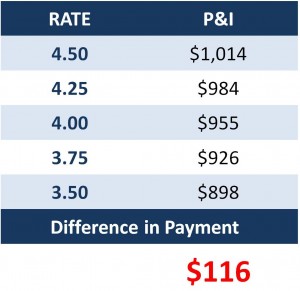

A big component in the cost of a home is the mortgage interest rate a purchaser pays. Understanding where rates are headed will help in making a decision whether to buy now or wait.

A big component in the cost of a home is the mortgage interest rate a purchaser pays. Understanding where rates are headed will help in making a decision whether to buy now or wait.