Shared with Permission:

Super Bowl Appearances vs. Real Estate Prices

Emmanuel Fonte | Music | Art | Leadership

If music be the food of love, play on. Emmanuel Fonte website is about music, art, real estate, architecture, design and decor. Occasionally, I talk about my other passion, hockey.

The REAL Trends Housing Market Report Video depicts national and regional trends for the residential real estate market. January report is based on Dec. 2012 Data.

The REAL Trends Housing Market Report Video depicts national and regional trends for the residential real estate market. January report is based on Dec. 2012 Data.

[pb_vidembed title=”” caption=”” url=”http://www.youtube.com/watch?v=qmxCbvnR2MY” type=”yt” w=”600″ h=”338″]

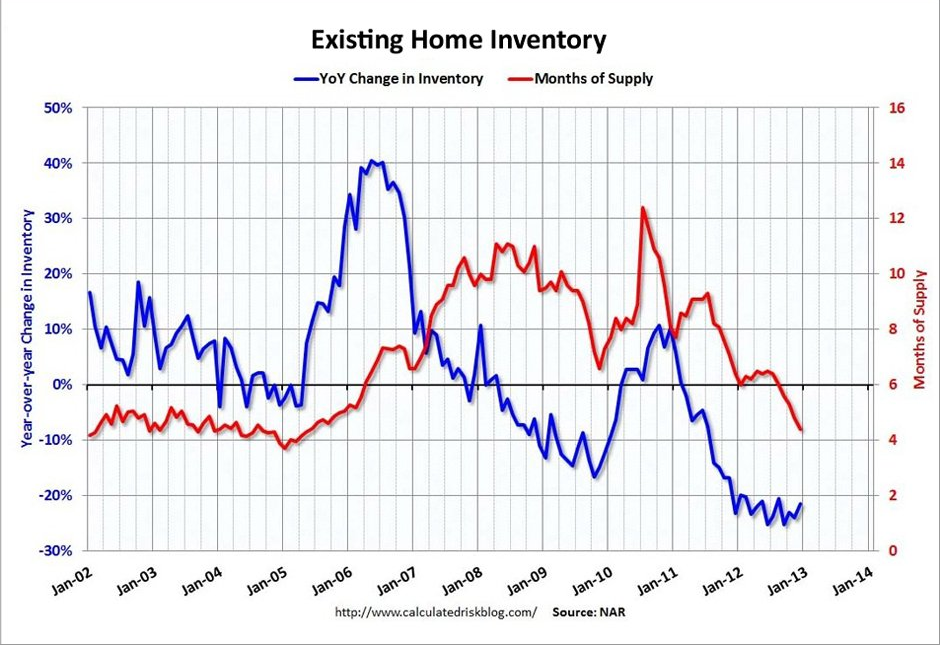

Home prices are increasing across the country as the number of homes for-sale continues to fall. But at a time when buyer demand is picking up, why is inventory still so low?

Home prices are increasing across the country as the number of homes for-sale continues to fall. But at a time when buyer demand is picking up, why is inventory still so low?

Inventories fell to 1.82 million at the end of last year, a 21.6 percent drop from one year earlier, the National Association of REALTORS® reports.

The Wall Street Journal recently highlighted several reasons behind the dropping inventories, including:

Source: “Six Reasons Housing Inventory Keeps Declining,” The Wall Street Journal

Today’s existing home sales number was a little weaker than expected.

Today’s existing home sales number was a little weaker than expected.

But have no fear, the housing comeback train continues.

Calculated Risk shows the number of months worth of existing home supply (red line). And that number continues to drop.

Which means: The price of your home is going to go up, as inventory gets tighter.

At this point, most people agree that the U.S. housing market is recovering.

At this point, most people agree that the U.S. housing market is recovering.

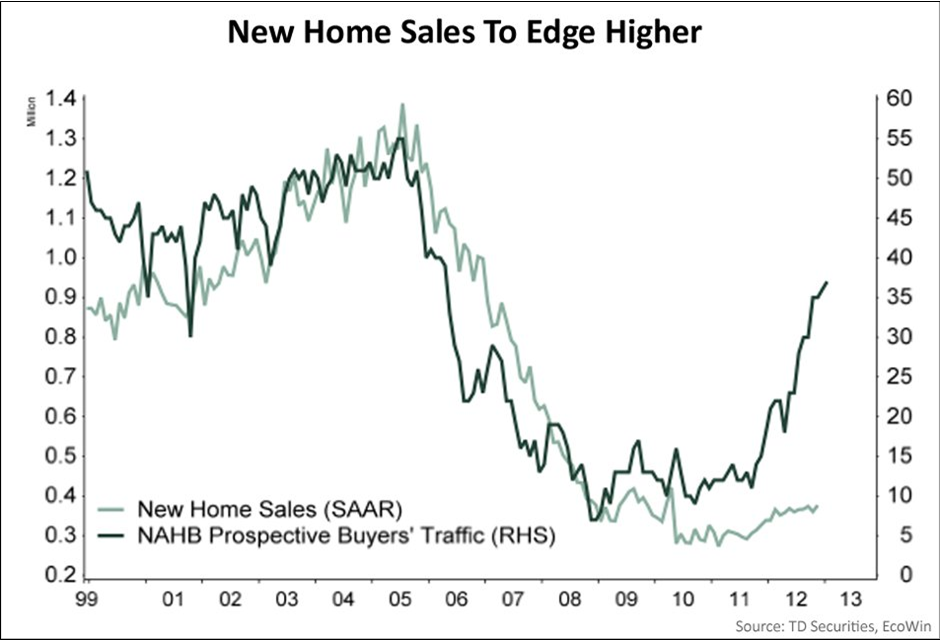

However, there continues to be one less-than-stellar metric of the housing market: new home sales.

The explanation for this is pretty intuitive. The economy is still anemic, and steep discounts are driving buyers to older existing homes.

Meanwhile, the homebuilders are increasingly optimistic and housing starts have been on the rise. This has some economists worried that a supply glut is building in the market for new homes.

Next Friday, we’ll get the latest reading of new home sales. Economists expect a healthy jump, which should help with this disconnect in the market.

Here’s TD Securities with some commentary:

The new homes market has been a laggard in the overall housing market recovery, and while new homebuilding and existing home sales activity have risen significantly from their lows, new home sales have yet to enjoy a similar turnaround in fortune. In December, we expect sales activity to improve only modestly, with the pace of sales boasting a respectable 6.1% m/m gain to 400K. The increase in sales will add to the positive momentum in November, when sales rose an equally impressive 4.4% m/m, justifying the surge in optimism among homebuilders (as seen in the NAHB homebuilders’ sentiment report) about sales prospects in recent months. In the coming months, we expect the positive momentum in new home sales activity to be sustained, though it is likely to continue to lag the buoyancy in the existing homes market.

Here’s TD’s chart. Hopefully, the increasing homebuyer traffic will eventually lead to a pick up in sales.

Read more: http://www.businessinsider.com/chart-new-homes-sales-lagging-2013-1#ixzz2INIRuDxQ

Builders broke ground on new homes in December at the fastest pace in more than four years offering a “solid ending to 2012 and a promising start to 2013,” according to the National Association of Home Builders.

Builders broke ground on new homes in December at the fastest pace in more than four years offering a “solid ending to 2012 and a promising start to 2013,” according to the National Association of Home Builders.

Housing starts soared 12.1 percent in December, reaching a 954,000 annual rate and the fastest pace since June 2008, the Commerce Department reported Thursday. Most of the jump was attributed to a 20.3 percent increase in multifamily construction last month, helping the sector return to a nearly normal production pace by historical standards. Housing starts for single-family homes rose 8.1 percent in December.

“With inventories of new homes at razor thin levels, builders are moving prudently to break ground on new construction ahead of the spring buying season to meet increasing demand,” says Barry Rutenberg, chairman of the National Association of Home Builders.

Permits for future home building — an indicator of future building — also rose slightly in December to its quickest pace since July 2008. Permits rose by the greatest amount in the Northeast by 19 percent and 6.6 percent in the West. The Midwest saw a 5.7 percent decline in housing permits, while the South saw a 3.4 percent decline in December.

Source: National Association of Home Builders and “Housing Starts Climb to Highest Rate Since June 2008,” Reuters

Americans are on the move again—at the highest level since before the recession. About 3.9 percent—or 11.8 million—of Americans moved to a different county in 2011, according to newly released Census data.

Americans are on the move again—at the highest level since before the recession. About 3.9 percent—or 11.8 million—of Americans moved to a different county in 2011, according to newly released Census data.While the number is improving, the percentage is still low by historical standards, but it is inching off record lows seen in 2009 and 2010. In 2010 and 2009, moves to different counties were about 3.5 percent—the lowest level since the government started tracking such data in 1948.

When people move between counties, they’re usually relocating due to jobs, according to Census demographers.

The 2011 increase is “one of the many indicators showing that the worst of the recession is probably over and we’re starting to inch back,” William Frey, a demographer at the Brookings Institution, told The Wall Street Journal.

The populations moving the most are 25-to-29 year olds—who have been “stymied by the weak labor market” in recent years, Frey says. “They’re the ones who’ve been stuck at home because of the economic downturn,” Frey said. “The so-called lost generation seems to have stirred a little bit.”

Also, another demographer notes, that retirees began to move more in 2011.

The states that gained the most in population in 2011 due to domestic moves were Florida and Nevada, according to the Census data.

Source: “Americans Get Moving Amid Torpid Recovery,” The Wall Street Journal

The housing market has shown signs of “bottoming out nationally and clearly turning a corner,” according to the Obama Administration’s December Housing Scorecard.

The housing market has shown signs of “bottoming out nationally and clearly turning a corner,” according to the Obama Administration’s December Housing Scorecard.Home values are inching up while home sales remain strong. Some home price indexes are showing values up 5.6 percent and 4.3 percent from year ago levels, according to the Scorecard.

“As the December housing scorecard indicates, our housing market is continuing to show important signs of recovery,” says Michael Berman, a HUD senior adviser.

Home inventories are falling, reaching a 4.8-month supply in December compared to November’s 5.3-month supply.

Americans are continuing to see the amount of equity in their homes increase. American home equity grew to $8 trillion in December but is still below the nearly $14 trillion in equity reached prior to the recession.

More than 6 million mortgage modifications and other kinds of housing assistance have taken place between April 2009 and November 2012, helping more home owners stay in their homes, according to the administration.

The housing scorecard is a comprehensive report on the national housing market, released every month by the U.S. Department of Housing and Urban Development and the U.S. Department of Treasury.

To view the complete Housing Scorecard, visit www.hud.gov/scorecard.

Source: The U.S. Department of Housing and Urban Development and “December Housing Scorecard Points to Improving Home Equity and Prices,” Mortgage News Daily

First-time home buyers are playing a larger role in the housing market, but they’re finding big changes.

First-time home buyers are playing a larger role in the housing market, but they’re finding big changes.

Thirty-nine percent of home sales nationwide were from first-time home buyers during the 12-month period ending June 2012, according to the National Association of REALTORS®. That’s up from 37 percent a year earlier.

But while first-time home buyers once had a huge inventory of homes to choose from, now they’re finding tightened supplies and steeper competition for what’s left.

Housing inventories are hovering at record lows in many markets, limiting supply. First-time home buyers face increased competition from investors, who are often trying to snatch up the same bargain-priced housing deals. Investors often make all-cash offers, too, which makes it difficult for buyers requiring financing to compete against them. Also, banks have tightened up their underwriting standards, creating more hoops in just qualifying for financing.

It’s not easy to be a first-time home buyer, some say. But first-time home buyers are critical to a healthy housing market. They allow existing home owners to sell and trade up into larger homes.

To respond to the changing housing market, first-time home buyers may need to broaden their search and be more “flexible and compromise,” says Chip Rowand, a Broward County, Fla., real estate professional.

Also, first-timers shouldn’t automatically settle for a Federal Housing Administration mortgage due to the low down payment requirements (usually 3.5 percent of the purchase price). The FHA can have several restrictions that makes some sellers prefer buyers who offer cash or who are using conventional loans, says Stephen B. McWilliam, president of Greater Fort Lauderdale (Fla.) REALTORS®. Some conventional loans require just 5 percent down and so may serve as an option for first-timers.

First-timers also need to be able to act fast and be able to have their financing processed quickly if they are going to stay competitive. Some banks won’t sign off on mortgages for eight to 12 weeks. But some sellers won’t wait that long. Some housing experts suggest first-timers look into working with a community bank or local mortgage banker, which often don’t have as long a wait.

Source: “First-time Home Buyers May Have to Compromise,” Sun Sentinel