One of the most interesting revelations of the latest National Association of Realtors (NAR) Existing Home Sales Report is the shortage of housing inventory being reported throughout much of the country. At the same time, buyer demand is dramatically up over last year. Here are some key points:

One of the most interesting revelations of the latest National Association of Realtors (NAR) Existing Home Sales Report is the shortage of housing inventory being reported throughout much of the country. At the same time, buyer demand is dramatically up over last year. Here are some key points:

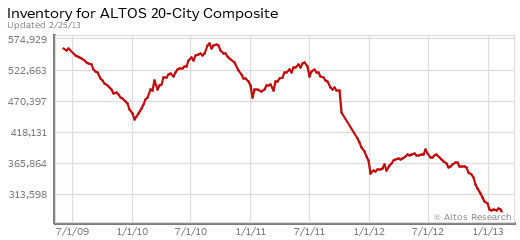

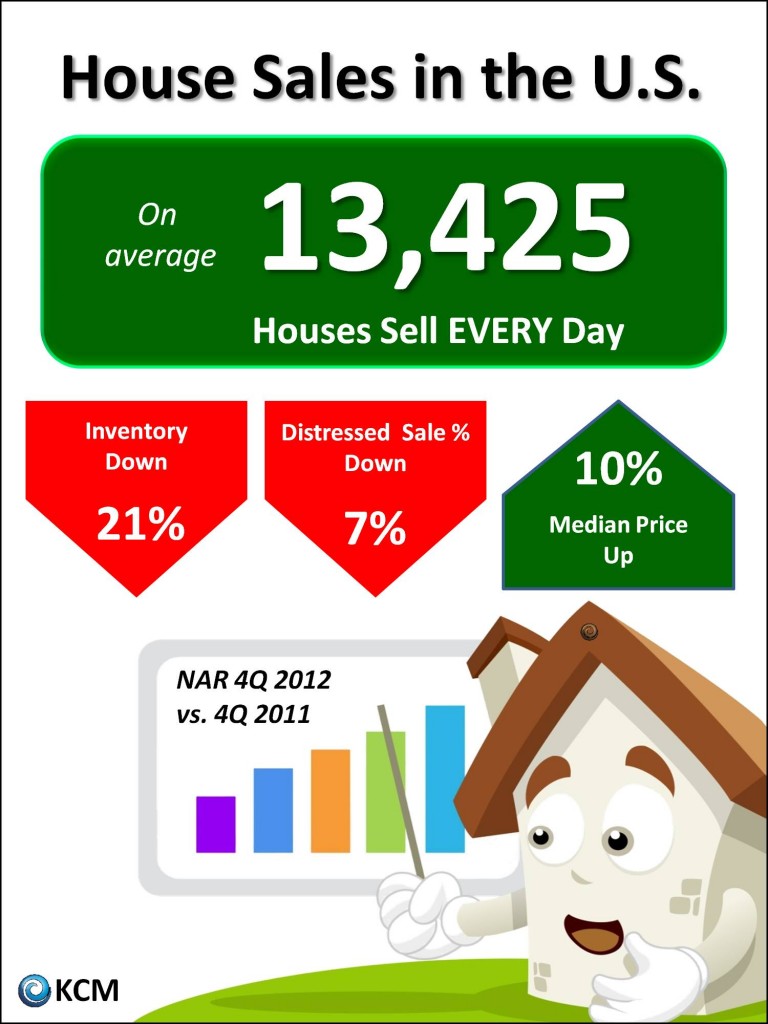

- Total housing inventory at the end of January fell 4.9 percent to 1.74 million existing homes available for sale, which represents a 4.2-month supply at the current sales pace.

- This represents the lowest housing supply since April 2005 when it was also 4.2 months.

- Listed inventory is 25.3 percent below a year ago when there was a 6.2-month supply.

- Raw unsold inventory is at the lowest level since December 1999 when there were 1.71 million homes on the market.

What Does This Mean if You Are Selling a Home?

The price of anything is determined by supply and demand. According to NAR’s report, inventory is at its lowest level since the real estate boom eight years ago. At the same time, demand is up. Lawrence Yun, NAR chief economist, reveals:

“Buyer traffic is continuing to pick up, while seller traffic is holding steady. In fact, buyer traffic is 40 percent above a year ago, so there is plenty of demand but insufficient inventory to improve sales more strongly. We’ve transitioned into a seller’s market in much of the country.”

Does that mean you should sell your house now? Or should you wait to see if prices increase? Nobody knows for sure. However, some feel that there may be a pent-up inventory about to come to the market because, as prices increase, it will free up some sellers who have been locked in a negative equity situation (where the house is worth less than the remaining mortgage).

The Zillow Negative Equity Forecast predicts:

“The negative equity rate among all homeowners with a mortgage will fall to at least 25.5 percent by the fourth quarter of 2013, freeing more than 999,000 additional homeowners nationwide.”

If these homes come to market, the supply/demand ratio will begin to balance out and lessen the opportunity a seller now has.

Calculated Risk, a well respected blog which analyzes the economy:

“With the low level of inventory, both in absolute numbers and as a month-of-supply, and the recent price increases in some areas, it would seem likely more inventory would come on the market.”

Lawrence Yun agrees:

“We expect a seasonal rise of inventory this spring.”

Yet, Yun is quick to add:

“It may be insufficient to avoid more frequent incidences of multiple bidding and faster-than-normal price growth.”

Probably the most interesting comment on this comes from Calculated Risk:

“I need to think about this…This will be an interesting issue all year.”

This is an issue that is important to every seller. Make sure that you are working with a true professional that is dedicated to keeping current on what matters in the real estate market so he/she may provide you with the best advice possible as this situation becomes clearer.